Dental crowns are one of the most common restorative procedures, but many patients wonder whether their insurance will help cover the cost. The answer depends on several factors, including your specific plan, the reason you need a crown, and whether the procedure is considered medically necessary or cosmetic. Understanding how dental crown insurance works can help you plan financially and make informed decisions about your oral health.

At TruSmile Now, Dr. Hanna Choi, DDS, provides comprehensive general and restorative dental care with a gentle, patient-centered approach. Dr. Hanna Choi focuses on helping patients maintain optimal oral health while ensuring every treatment is tailored to their unique needs and delivers the best possible outcome.

Most dental insurance plans categorize crowns as a major restorative procedure, which typically means they fall under a different coverage tier than routine cleanings or fillings. While preventive care is often covered at 100%, major procedures like crowns are usually covered at 50% to 80% of the total cost, depending on your plan. However, this coverage only kicks in after you have met your annual deductible, and it is subject to your plan’s annual maximum benefit limit.

💰 HOW DENTAL CROWN INSURANCE COVERAGE WORKS

Understanding dental crown insurance requires familiarity with how dental plans are structured. Most plans divide services into three categories: preventive, basic, and major. Crowns fall into the major category, which means they receive lower reimbursement rates compared to routine procedures. Your insurance company will typically cover a percentage of the allowed amount for the crown, leaving you responsible for the remaining balance.

The amount your insurance pays depends on several key factors. First, there is the annual deductible, which is the amount you must pay out of pocket before your insurance begins covering services. Deductibles for dental plans typically range from $50 to $150 per person. Once you meet this deductible, your insurance will begin paying its portion of covered services.

Second, there is the coinsurance percentage. For major procedures like crowns, most plans cover 50% of the cost, though some more comprehensive plans may cover up to 80%. This means if your crown costs $1,200 and your plan covers 50%, you would be responsible for $600 plus any amount exceeding your annual maximum.

Third, every dental insurance plan has an annual maximum benefit, which is the most your insurance will pay for dental care in a given year. This limit typically ranges from $1,000 to $2,000. Once you reach this maximum, you are responsible for 100% of any additional dental costs for the remainder of the year. According to the American Dental Association, understanding your plan’s annual maximum is crucial for budgeting dental care throughout the year.

🦷 WHEN IS DENTAL CROWN INSURANCE MORE LIKELY TO COVER YOUR CROWN?

Insurance companies evaluate whether a crown is medically necessary based on the condition of your tooth. Dental crown insurance is more likely to provide coverage when the crown is needed to restore function, protect a damaged tooth, or prevent further decay. Crowns placed for purely cosmetic reasons are rarely covered by insurance.

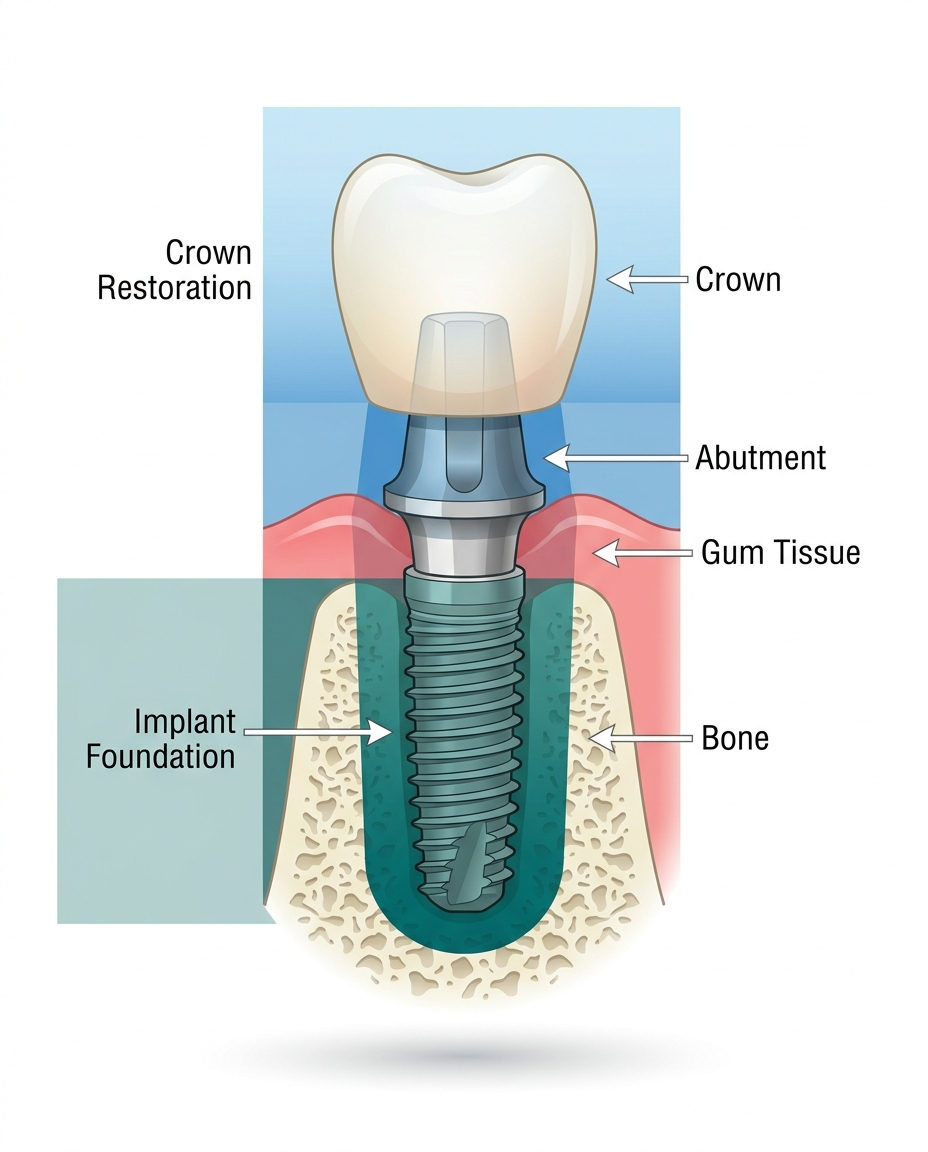

Common scenarios where insurance typically covers crowns include teeth that are severely decayed, cracked, or broken. If a tooth has undergone a root canal, a crown is often necessary to protect the weakened structure, and insurance usually covers this. Crowns used to anchor a dental bridge or restore a dental implant are also frequently covered, as they serve a functional purpose.

However, if you want a crown to improve the appearance of a healthy tooth, such as covering discoloration or reshaping a tooth for aesthetic reasons, your insurance is unlikely to pay. In these cases, the procedure is considered elective cosmetic dentistry. Some plans may also have waiting periods before they will cover major procedures like crowns, especially if you recently enrolled in a new plan. Waiting periods typically range from 6 to 12 months.

It is also important to know that some insurance plans have frequency limitations. For example, your plan may only cover one crown per tooth every 5 to 7 years. If you need to replace a crown before this time frame, you may have to pay the full cost out of pocket unless there is documented evidence that the crown failed due to no fault of your own.

📋 TYPES OF DENTAL INSURANCE PLANS AND CROWN COVERAGE

Not all dental insurance plans are created equal. The type of plan you have significantly impacts how much coverage you receive for crowns. The most common types of dental insurance include PPO plans, HMO plans, indemnity plans, and discount dental plans. Each has different rules regarding dental crown insurance and out-of-pocket costs.

PPO (Preferred Provider Organization) Plans

PPO plans are the most popular type of dental insurance. They offer a network of preferred dentists who have agreed to charge reduced fees for services. If you visit an in-network dentist, your insurance will cover a higher percentage of the cost. PPO plans typically cover crowns at 50% to 80% after you meet your deductible. You can visit out-of-network dentists, but your coverage will be lower, and you may face higher out-of-pocket costs.

HMO (Health Maintenance Organization) Plans

HMO dental plans require you to choose a primary dentist from within the network. You must receive all care from this dentist unless you get a referral to a specialist. HMO plans often have lower premiums and no deductibles, but they may have more restrictions on coverage. Crowns are typically covered, but you may have limited options regarding the type of crown material used.

Indemnity Plans

Indemnity plans, also known as traditional or fee-for-service plans, allow you to visit any dentist you choose. The insurance company pays a set percentage of the dentist’s fee, and you pay the rest. These plans offer the most flexibility but often have higher premiums and deductibles. Coverage for crowns is similar to PPO plans, typically 50% of the cost.

Discount Dental Plans

Discount dental plans are not insurance. Instead, you pay an annual membership fee to access reduced rates at participating dentists. These plans do not have deductibles, annual maximums, or waiting periods. While they do not provide dental crown insurance coverage, they can reduce the cost of a crown by 10% to 60% depending on the plan and provider.

💡 WHAT TO DO IF YOUR INSURANCE DOES NOT COVER CROWNS

If your insurance does not cover crowns or if your coverage is limited, you still have options to make treatment affordable. Many dental practices, including TruSmile Now, offer flexible payment solutions to help patients access the care they need without financial stress.

One option is to use a Health Savings Account (HSA) or Flexible Spending Account (FSA). Both accounts allow you to set aside pre-tax dollars for medical and dental expenses, including crowns. Using an HSA or FSA can reduce the effective cost of your crown by avoiding taxes on the money used to pay for it. According to research published in the Journal of Dental Research, patients who utilize tax-advantaged accounts report lower financial barriers to receiving necessary dental care.

Another option is financing through third-party providers. We offer flexible payment plans through Cherry to make treatment affordable. These plans allow you to spread the cost of your crown over several months with low or no interest, making it easier to fit dental care into your budget.

Some patients also consider dental schools or community health centers, where dental students provide care under the supervision of experienced dentists. While this can reduce costs, it may also extend treatment time and limit your choice of providers.

📞 HOW TO VERIFY YOUR DENTAL CROWN INSURANCE COVERAGE

Before scheduling your crown procedure, it is essential to verify your coverage to avoid surprises. Start by contacting your insurance company directly or reviewing your plan documents. Ask specific questions about your dental crown insurance benefits, including your deductible, coinsurance percentage, annual maximum, and any waiting periods or frequency limitations.

You should also ask whether your dentist is in-network. In-network dentists have negotiated rates with your insurance company, which can significantly reduce your out-of-pocket costs. At TruSmile Now, we accept most major insurance plans, including Delta Dental, Cigna, UnitedHealthcare, MetLife, Aetna, BCBS, and more. Our team can help you verify your benefits and provide a detailed estimate of your costs before you begin treatment.

Another important step is to request a predetermination or preauthorization from your insurance company. This involves your dentist submitting a treatment plan to your insurance company before the procedure. The insurance company reviews the plan and provides a written estimate of what they will cover. While this is not a guarantee of payment, it gives you a clearer picture of your expected costs.

🏆 WHY CHOOSE TRUSMILE NOW FOR YOUR DENTAL CROWN

At TruSmile Now, we understand that navigating dental crown insurance can be confusing and stressful. That is why our team is dedicated to helping you understand your benefits and maximize your coverage. We work with most major insurance providers and will handle the paperwork and claims process on your behalf.

One of our unique advantages is our state-of-the-art in-house dental lab. This allows us to create custom crowns on-site, often in a single visit, reducing the time you spend in the dental chair and eliminating the need for temporary crowns. Our in-house lab also gives us greater control over quality and fit, ensuring your crown looks natural and functions properly.

We also offer a New Patient Special for just $49, which includes a comprehensive exam, X-rays, and consultation. This is a great opportunity to discuss your crown needs, review your insurance coverage, and develop a personalized treatment plan that fits your budget.

If cost is a concern, we offer flexible payment plans through Cherry, allowing you to spread the cost of your crown over time with low monthly payments. We believe everyone deserves access to quality dental care, regardless of their insurance situation.

❓ FREQUENTLY ASKED QUESTIONS

Does dental crown insurance cover cosmetic crowns?

Most dental insurance plans do not cover crowns placed for purely cosmetic reasons. Insurance typically only covers crowns that are medically necessary to restore function, protect a damaged tooth, or prevent further decay. If you want a crown to improve the appearance of a healthy tooth, you will likely need to pay the full cost out of pocket.

How much does dental crown insurance typically pay for a crown?

Most dental insurance plans cover 50% to 80% of the cost of a crown after you meet your annual deductible. The exact percentage depends on your specific plan and whether your dentist is in-network. You are responsible for the remaining balance, as well as any costs that exceed your plan’s annual maximum benefit.

Can I get a crown if I have not met my deductible?

Yes, you can still get a crown even if you have not met your deductible. However, you will need to pay the deductible amount out of pocket before your insurance begins covering its portion of the cost. Deductibles for dental plans typically range from $50 to $150 per person.

What if my insurance has a waiting period for crowns?

Many dental insurance plans have waiting periods for major procedures like crowns, especially if you recently enrolled. Waiting periods typically range from 6 to 12 months. If your tooth needs immediate treatment, you may need to pay out of pocket or explore financing options until your waiting period ends.

Does Medicare cover dental crowns?

Original Medicare (Parts A and B) does not cover routine dental care, including crowns. However, Medicare Part B may cover dental services that are medically necessary as part of another covered procedure, such as jaw reconstruction after an accident. Some Medicare Advantage plans (Part C) offer dental benefits that may include coverage for crowns. At TruSmile Now, we accept Medicare Part B for medically necessary treatments.

How can I reduce the cost of a crown without insurance?

If you do not have insurance or your coverage is limited, you can reduce the cost of a crown by using an HSA or FSA, enrolling in a discount dental plan, or taking advantage of financing options. At TruSmile Now, we offer flexible payment plans through Cherry to help make your crown affordable.

📍 VISIT TRUSMILE NOW – 3 ARIZONA LOCATIONS

TruSmile Now Peoria

20542 N Lake Pleasant Rd, Suite 113

Peoria, AZ 85382

Phone: (602) 362-0447

Hours: Mon-Thu 9:00 AM – 5:00 PM

TruSmile Now Chandler

2900 W Ray Rd #3

Chandler, AZ 85224

Phone: (480) 393-0687

Hours: Mon-Thu 9:00 AM – 5:00 PM

TruSmile Now Ahwatukee (Phoenix)

4530 E Ray Rd #170

Phoenix, AZ 85044

Phone: (480) 360-4754

Hours: Mon 9-5, Tue 7am-2pm, Wed-Thu 10-7, Fri 8-3, Sat 8am-1pm

Serving Peoria, Chandler, Ahwatukee, Phoenix, Tempe, Mesa, Gilbert, Scottsdale, Glendale, Surprise, and the Greater Phoenix metro area.

New Patient Special: $49 – Includes exam, X-rays, and consultation!

We accept most major insurance including Delta Dental, Cigna, UnitedHealthcare, MetLife, Aetna, BCBS, and more. Medicare Part B accepted for medically necessary treatments.

We offer flexible payment plans through Cherry to make your treatment affordable.

Have a quick question before booking? Lucy is our AI assistant who is always online. Just start a chat and she will point you in the right direction.

Ready to learn more about dental crown insurance and your coverage options? Call any of our locations or schedule online today!

View our before and after gallery to see real patient results!